A recent paper in the journal Mathematics explores the potential of a hybrid quantum-classical model. This innovative approach integrates a quantum layer into a traditional neural network to enhance credit scoring accuracy.

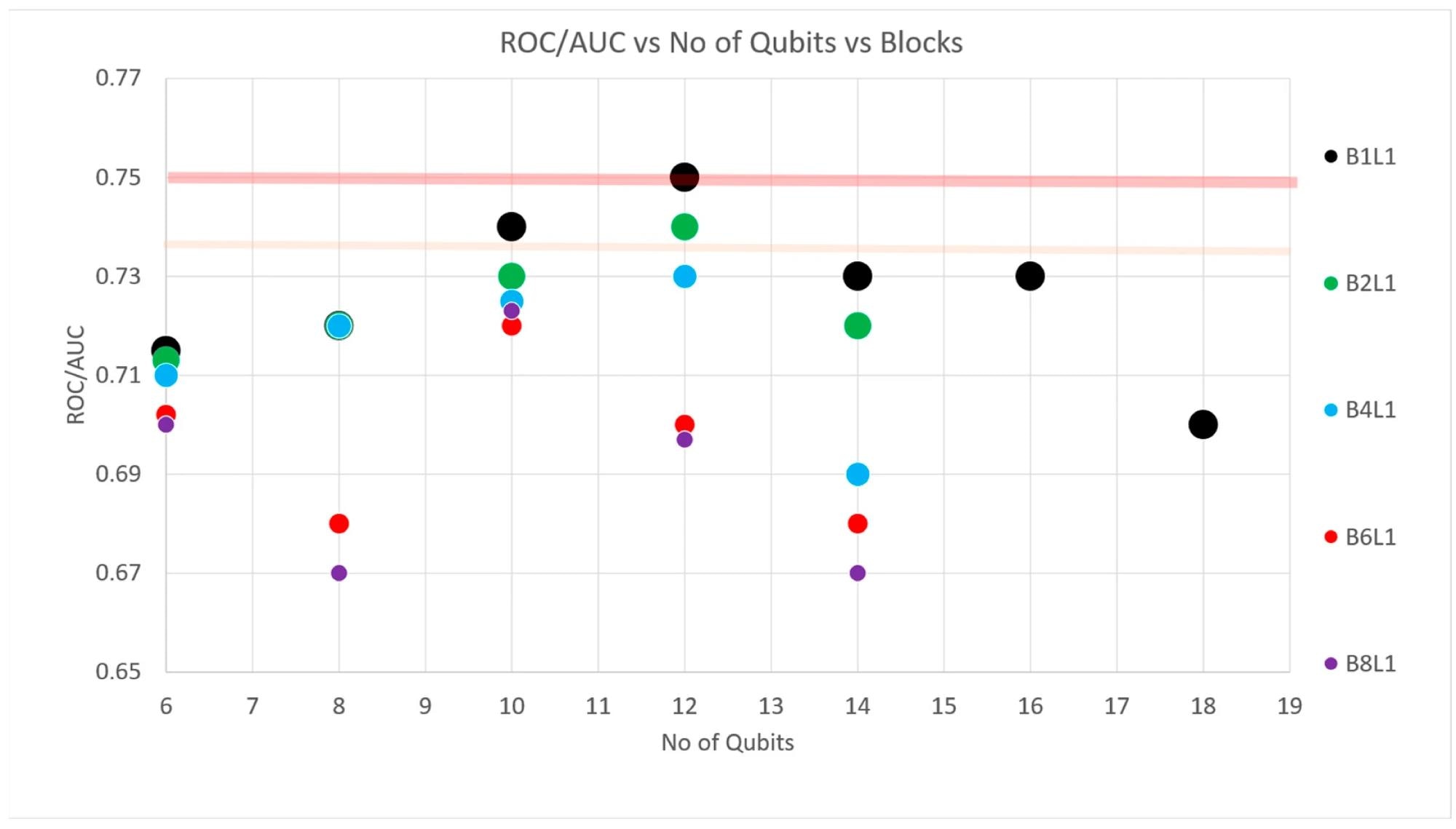

The FH model versus the number of qubits (x-axis) and number B of blocks (colored circles). The orange line denotes the classical counterpart model ROC/AUC when trained for a maximum of 350 epochs, while the red line denotes the classical counterpart model’s ROC/AUC when trained for a maximum of 3500 epochs. Image Credit: https://www.mdpi.com/2227-7390/12/9/1391

The FH model versus the number of qubits (x-axis) and number B of blocks (colored circles). The orange line denotes the classical counterpart model ROC/AUC when trained for a maximum of 350 epochs, while the red line denotes the classical counterpart model’s ROC/AUC when trained for a maximum of 3500 epochs. Image Credit: https://www.mdpi.com/2227-7390/12/9/1391

Importance of Quantum Machine Learning

The investigation of quantum physics in the context of finance—termed quantum finance—has demonstrated its relevance in several key areas such as risk analysis, portfolio optimization, and option pricing. Quantum finance employs quantum machine learning and quantum computing to address complex financial computations including market trend analysis and risk management.

The focus of this research is on credit scoring, an essential financial function with significant economic implications. Extensive research has been conducted to enhance machine learning models for credit scoring, particularly for small and medium-sized enterprises (SMEs). Despite advancements, current models frequently misjudge insolvency, leading to the wrongful rejection of numerous solvent businesses.

Modest improvements to these models can decrease erroneous rejections and substantially reduce risks for lenders. Such enhancements can be realized through the application of quantum machine learning, which combines quantum computing with machine learning to refine financial analysis.

Quantum machine learning can significantly expedite data analysis by utilizing quantum physics principles. Pursuing heuristic algorithms that perform well in specific problem areas through domain expertise and cross-disciplinary insights—despite lacking formal theoretical foundation—is vital for advancing quantum machine learning in financial applications.

The Proposed Approach

In this study, researchers explored the integration of quantum circuits with classical neural networks to enhance credit scoring methodologies for SMEs. They developed a new architecture that combines quantum variational circuits (VCs) with data re-uploading classifiers (DRCs) within a hybrid classical-quantum neural network. This model was tested using a credit default dataset from nearly 2,300 SME firms in Singapore, incorporated between 1940 and 2016.

The proposed heuristic approach, termed the FULL HYBRID (FH) classical-quantum neural network model, focuses on leveraging the synergies between classical and quantum computational models. Its performance was benchmarked against a purely classical machine learning model, referred to as the classical counterpart (CC), to demonstrate the efficacy of quantum machine learning in credit scoring.

The selection of SMEs for this study was driven by their typical lack of formal credit ratings, aiming to improve predictive accuracy in financial contexts and to explore both practical applications and theoretical limits of quantum-enhanced data analysis. In the FH model, the architecture consists of an initial classical neural network (NN) followed by the VC-DRC circuit and concludes with a decision layer featuring a single neuron with a sigmoid activation function.

The classical NN part includes a two-neuron layer with a rectified linear activation function (ReLU), referred to as the master classical layer, followed by another two-neuron layer with a Leaky ReLU activation function, known as the feeding classical layer. The prediction is ultimately made by the classical decision layer, also known as the final decision layer.

To prevent overfitting, a dropout layer with a rate of 10% was incorporated after every classical layer in both the CC and quantum models. Angle embedding was utilized for encoding data into quantum states. Data preprocessing involved a standard pipeline and proprietary processing before being fed into the models. The experiments were conducted using simulators, ensuring that quantum computer noise was non-existent and no additional noise was introduced.

Evaluation and Findings

The performance of the quantum model was evaluated against the CC model, and versus the number of blocks and the number of qubits. Researchers used the same testing, training, and validation dataset throughout the simulations.

Additionally, the average outcome of the receiver operating characteristic (ROC)/area under the ROC curve (AUC) score of five simulations was used for every configuration. To ensure a fair comparison, the number of epochs for both classical and quantum models was kept at 350.

Results showed that the incorporation of a quantum layer into a traditional neural network led to significant reductions in training time. The proposed NN/VC-DRC hybrid model achieved efficient training with significantly fewer epochs compared to its CC counterpart for a similar predictive accuracy.

For instance, the FH model achieved an ROC/AUC of 0.75 with 350 epochs, while the CC model achieved the same ROC/AUC score of 0.75 with 3500 epochs. Similarly, the FH model's performance was influenced by the changes in the number of blocks and qubits.

For instance, the ROC/AUC of the FH increased up to 12 qubits and then decreased after 12 qubits for blocks = 1. The same behavior was observed when the number of blocks was increased, with the highest results/best performance being achieved with no data re-upload.

To summarize, the findings of this study demonstrated that the proposed quantum-classical hybrid model for credit scoring has significant potential in the financial sector. However, two critical challenges, including the overparameterization problem and barren plateau phenomenon within quantum circuits, that can affect the accuracy must be addressed for advancing the use of quantum machine learning algorithms in practical applications.

Journal Reference

Schetakis, N., Aghamalyan, D., Boguslavsky, M., Rees, A., Rakotomalala, M., Griffin, P. R. (2024). Quantum Machine Learning for Credit Scoring. Mathematics, 12(9), 1391. https://doi.org/10.3390/math12091391, https://www.mdpi.com/2227-7390/12/9/1391

Disclaimer: The views expressed here are those of the author expressed in their private capacity and do not necessarily represent the views of AZoM.com Limited T/A AZoNetwork the owner and operator of this website. This disclaimer forms part of the Terms and conditions of use of this website.

Article Revisions

- May 10 2024 - Title changed from "Hybrid Quantum-Classical Model for Improved Credit Scoring" to "Quantum Finance Systems and Their Impact on Credit Scoring for SMEs"